Insurance carriers are fleeing states with known wildfire risk, notably California, leaving homeowners and states to grapple with what's next. Vibrant Planet knows we can strategically and measurably reduce wildfire risk, protecting built and natural systems, and render insurance products affordable and accessible.

Key Takeaways

- Insurance and climate risks are linked. Wildland fires cost homeowners, states, regions and insurers billions; big providers like State Farm and Allstate are backing away from insuring fire-prone states like California, Washington, and Oregon.

- The insurance market faces compounding challenges. Rules aimed at protecting consumers from price spikes might not align with rapidly changing climate risks, such as regulations preventing pricing future risk into annual fees.

- Fire mitigation reduces risk and can bring down insurance costs. In a recent project in which Vibrant Planet engaged, fire treatments reduced the probability of fire impacting structures in a Sierra Nevada community by 90-100%.

What’s going on? The insurance crisis

This week, insurance experts, decision-makers and stakeholders gathered in Los Angeles for the Inaugural Global Sustainable Insurance Summit. Summit attendees recognized the need for new approaches to embed the reality of climate change into insurance products, and clamored for policy, science and innovation to merge faster to realize that end goal. This event magnifies what we already know: the climate crisis is quickly igniting an insurance crisis. California made headlines last year when State Farm and Allstate, two major insurers, announced they would no longer issue new policies across the State. Thousands of residents in Washington, Oregon and California were all issued higher-priced renewals last fall, smaller insurers also departed California, and State Farm took things further by recently announcing it would not renew 72,000 policies in California.

States are now grappling with expanding enrollment in FAIR (Fair Access to Insurance Requirements) Plans, which provide basic fire insurance coverage when traditional companies will not. But California faces a Catch-22 – the FAIR Plan is not supported by taxpayers, but by all of the carriers licensed to do business in California. So as insurers leave, homeowners fall back to less comprehensive, costlier policies under the FAIR Plan, which is simultaneously being drained due to less revenue from fleeing insurers, creating enormous risk for homeowners. The FAIR Plan is not a fall back plan, it is merely one more seat to fill until the music stops.

Additionally, the loss of insurance produces ripple effects throughout communities, industries and the State. When home-buyers cannot complete a home purchase because they can’t secure insurance, they can’t take jobs near new homes, employ electricians, plumbers and solar companies to upgrade homes, or pay property taxes to the cities where the homes sit. Dial this up times a million and the ripple effect becomes a tsunami.

California needs a new insurance approach that holistically and transparently prices existing and future risk, with feasible paths for consumers to reduce their costs through household and community risk mitigation projects. Fortunately, the California Department of Insurance, led by Commissioner Ricardo Lara, is hitting the problem head on, producing directives and hosting this week’s Insurance Summit..

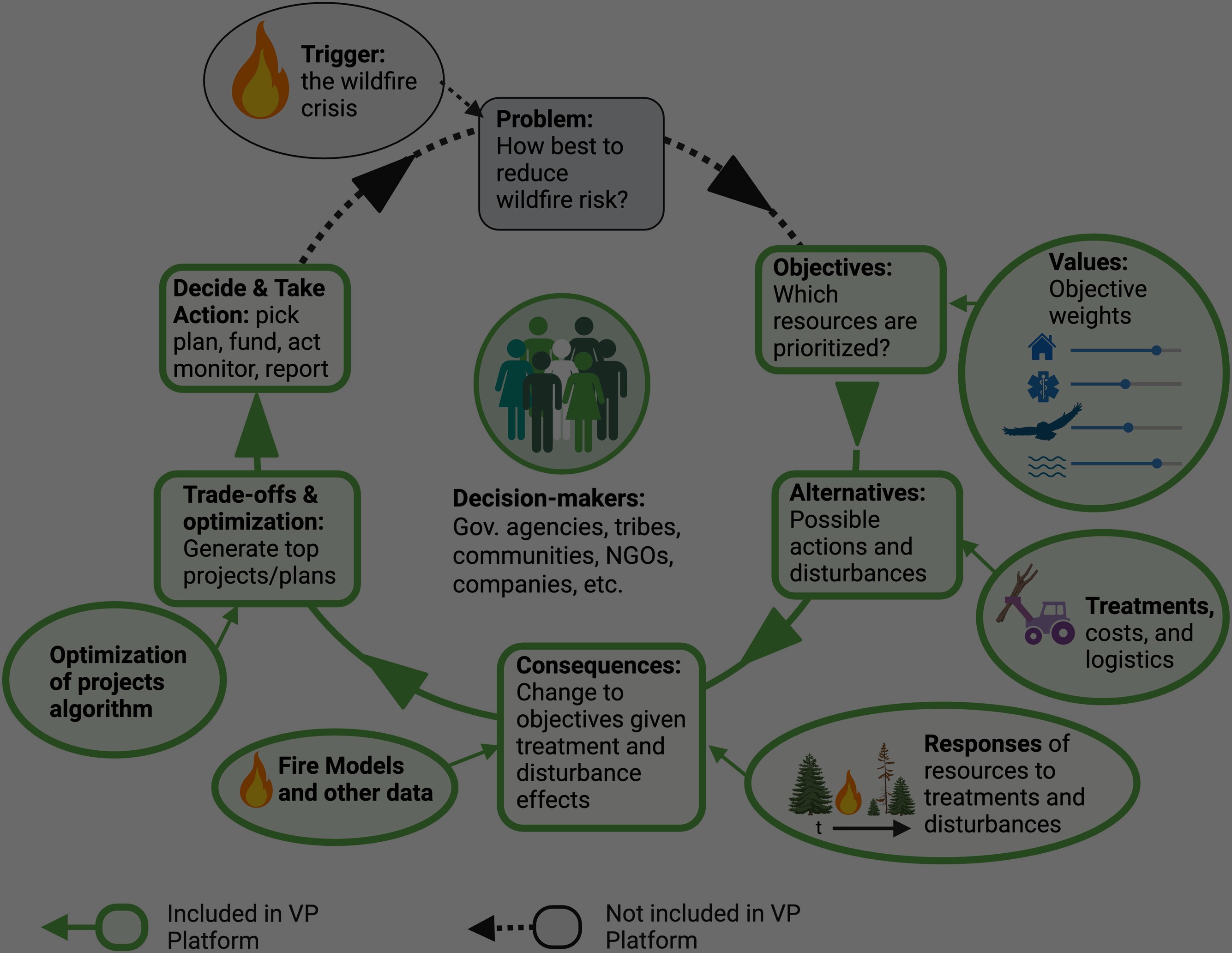

We know the solution for wildfires: if we scale strategic wildfire mitigation throughout our wildland forests, the wildland urban interface (WUI), and around our homes, we can reduce wildfire risk and appropriately price that reduction, keeping insurance achievable and accessible.

Compounding insurance price challenges

As insurers leave California and threaten to leave many other states with wildfire risk, rates increase for available policies due to dwindling insurance supply. Additionally, regulations to meaningfully protect consumers from price spikes may now be out of alignment with rapidly changing climate risks; for example, insurers can use proprietary data collected about past risk and household behavior, but may not use predictive catastrophe models to set rates (although lawmakers in California are advocating for a change). Regulations also prevent passing through reinsurance costs to customers. These rules are also colliding with inflation, building materials shortages and construction workforce shortages, producing an untenable market for homeowners and insurers alike. As panelist Newsha Ajami, Chief Strategic Development Officer for Research at Lawrence Berkeley National Lab explained at this week’s consortium, “We have 20th century policies and solutions that are supposed to address 21st century problems.”

Compounding these market and regulatory risks, longer wildfire seasons, more destructive fires, flooding, and sea level rise have led to drastic increases in claims and mounting economic losses. The 2020 wildfire season alone is estimated to have produced between $5 billion and $9 billion in destruction, following 2017 and 2018 wildfire seasons that each produced more than $10 billion in insured losses.

We know how to measurably reduce wildfire risk and retain insurance

With natural disasters such as flooding, damage from hurricanes, or destruction from drought or earthquakes, we can prepare for the worst but we cannot actively alter the trajectory or intensity of the event (save an international, concerted effort to dramatically reduce global carbon dioxide emissions). However, individual and collective action can directly reduce the risk profile of wildfires. According to the California Fire Science Consortium, forest fuel reduction treatments can alter the intensity and direction of a catastrophic wildfire - with great implications on the cost and geographic viability of insurance coverage.

For example, for the North Yuba Forest Partnership project in the Sierra Nevada, community members and forest managers used Vibrant Planet to collaboratively understand and prioritize forest management treatments to greatly reduce fire risk. These ecological forestry treatments include removing dead and dying trees and underbrush, creating fire lines and defensible space, removing invasive species, introducing prescribed fire in the right conditions, and otherwise aiming for forest health outcomes that protect both communities and the forest. The scenarios that Vibrant Planet helped community members and forest managers plan do not touch every acre of the forest, rather the community identified select treatments with higher forecasted benefits. Those forecasting benefits include:

- 90-100% risk reduction to structures in Downieville and Sierra City–the most populated areas within this landscape

- 90-100% reduction of burn probability in Downieville and Sierra City

Ecological forestry delivers staggering savings

By reducing the intensity and probability of fires through ecological forestry, land managers can have a direct effect on the cost of insuring homes in fire prone areas. According to a study by the Nature Conservancy on Wildfire Resilience Insurance, ecological forestry on the full North Fork American River sub-basin showed savings of 41% or ~$211M in aggregate annual home insurance premiums. Premium savings results of 52% for home insurance accounting for ecological forestry were obtained when analyzing a single community of 533 homes in the watershed.

These treatments also support more effective suppression of wildfires by reducing surface fuel load and allowing aerial fire-retardant drops to penetrate fires due to increased canopy openings; reduce the likelihood of structures being destroyed or damaged by wildland fires in nearby communities; and promote safer travel for both the public and firefighters.

For example, the 2021 Caldor Fire burned at 45% intensity, but a Caples Lake treatment completed by the Sierra Nevada Conservancy, the El Dorado Irrigation District and El Dorado National Forest two years prior to Caldor’s run left the Caples Lake watershed largely intact. It burned consistent with a natural fire regime and protected the watershed for water users downstream. These strategic treatments work and protect insured assets with real value.

Vibrant Planet and Pyrologix as part of the insurance solution

Vibrant Planet and Pyrologix produce detailed maps and data that identify potential fire ignitions and the intensity of those potential ignitions at tree level scales. This fine scale data underpins the analytics we provide to prioritize effective and cost-efficient ecological forestry treatment plans that measurably reduce fire risk in built environments, the WUI and wildlands. Where implemented, these actions can produce “community hardening,” as opposed to “home hardening” or “defensible space,” producing community level wildfire risk reduction that confers benefits to all the structures in the community. Community hardening will help insurers immediately write policies to all the homes in an area with greater certainty of risk abatement.

Vibrant Planet is actively engaging with California officials, academics, national industry groups, insurance and reinsurance companies to produce advanced analytics, and brainstorm financing and cross-sector actions that can improve insurance access in California, and in every other state currently threatened by catastrophic wildfire.

Our team, with expertise in data, policy, insurance, and product development, is part of local, regional, state and national partnerships, dedicated to:

- Mapping landscapes at the tree level using space-based and ground-collected data to identify wildfire risk potential and intensity in developed, WUI, and wildland areas;

- Delivering our applications to help communities plan treatments to mitigate and reduce wildfire risk, monitor treatment impact and quantify fire risk reduction to demonstrate insurance viability;

- Measuring potential reductions in flame length and ember cast as a result of wildfire mitigation treatments in developed, WUI and wildland areas;

- Monitoring forest treatment effectiveness. reporting actual reductions in wildfire intensity due to those treatments, and quantifying effectiveness of treatments on ignition risk probability and fire severity;

- Spurring new insurance products that can catalyze community hardening treatments, reduce risk and bring insurance back to the communities that need it most; and

- Developing innovative insurance models (like community embedded insurance) and regulatory approaches as critical elements of evolving insurance in the face of worsening wildfire and climate change.

Ultimately, we aim to lower risks in a community so that previously uninsurable communities may be insurable, insurance can be affordable for all, and the number/value of homes an individual insurer is willing to write in a given area increases.